How S Corp Basis Works (and Why It Matters): The 2026 Owner's Guide

S Corp basis explained in plain English. Stock basis vs. debt basis, what increases and decreases it, the AAA, Form 7203, distributions in excess of basis, and the mistakes that cost owners thousands.

If you've owned an S Corp for more than about 18 months, your CPA has probably said the word "basis" at you. And you, like most S Corp owners, probably nodded along while quietly wondering what they meant.

S Corp basis is one of those topics that sounds technical, gets explained badly in most articles, and ends up biting owners in the most expensive way: in the form of unnecessary capital gains tax, disallowed losses you should have been able to deduct, and a distribution that turns out to be taxable when you assumed it was free.

This guide walks through S Corp basis the way we'd explain it to a new client: what it is, why it matters, how to track it, what increases and decreases it, the difference between stock basis and debt basis, the role of the Accumulated Adjustments Account (AAA), how Form 7203 fits in, and the specific mistakes that cost owners real money. With a multi-year worked example so you can see basis in motion.

Let's untangle it.

The 60-Second Version

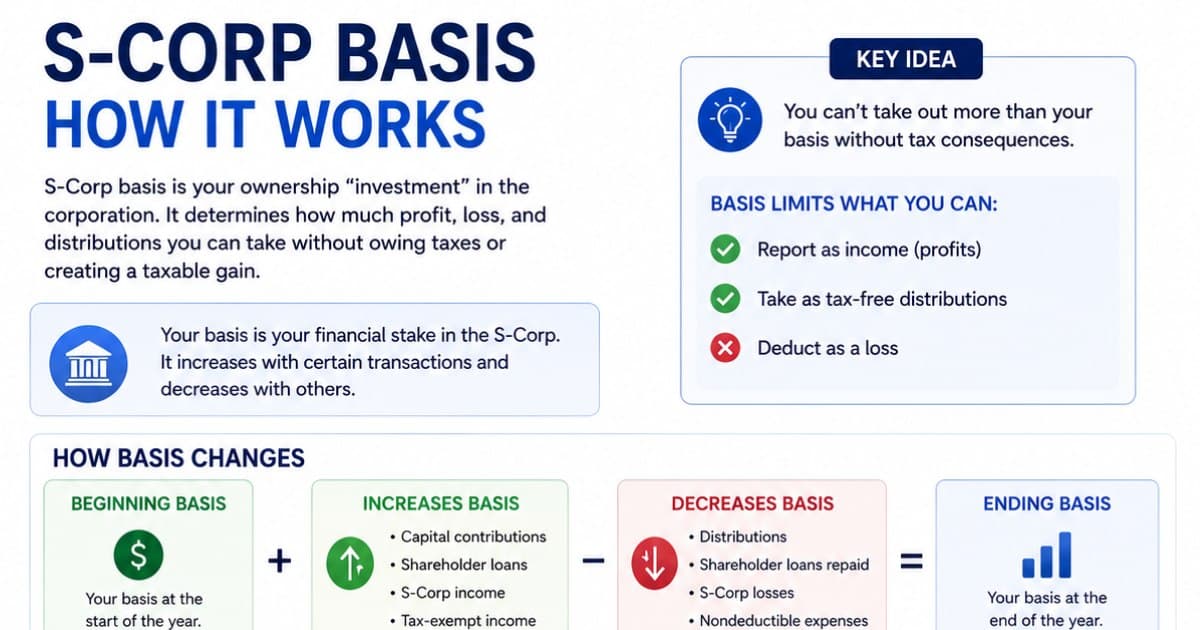

Your basis in an S Corp is, roughly, your investment in the company for tax purposes. It tracks how much money is "yours" inside the company.

Why it matters in three bullets:

- You can only deduct losses up to your basis. Losses beyond your basis are suspended and carried forward.

- Distributions are tax-free up to your basis. Distributions that exceed your basis become taxable capital gains.

- Your basis becomes the cost basis of your stock when you sell or liquidate the company. Higher basis = lower gain on sale.

Get basis wrong and you can either (a) miss legitimate loss deductions, (b) accidentally trigger capital gains on what should have been a tax-free distribution, or (c) miscalculate gain or loss when you eventually exit.

S Corps actually have two types of basis: stock basis (your investment in the equity) and debt basis (loans you personally made to the corporation). Both work similarly but track separately.

That's the headline. Now the detail.

Why Basis Exists at All

S Corp basis exists because S Corps are pass-through entities. Profits and losses flow to the owners' personal returns, distributions flow back out, and the government needs a way to track how much each shareholder has actually invested vs. how much they've already pulled out.

Without basis, an owner could:

- Deduct unlimited losses on their personal return (even more than they ever invested), creating artificial tax shelters.

- Take unlimited distributions tax-free (because distributions are non-taxable to the extent of AAA), even after the company has lost money or has paid out more than it earned.

- Sell their shares without any way to compute gain or loss.

Basis is the IRS's way of keeping the math honest. It's a running balance of "how much economic skin you have in the game" that goes up when you put money in or earn profit and goes down when you take money out or absorb losses.

Stock Basis vs. Debt Basis

S Corps have two distinct basis accounts for each shareholder.

Stock Basis

This is the bigger and more important one. Your stock basis represents your equity investment in the corporation.

Stock basis starts with whatever you paid for the stock — the cash you contributed when you formed the corporation, plus the fair-market-value basis of any property contributed.

For an LLC that elected S status from formation: your initial stock basis is whatever capital you contributed at formation.

For a corporation that converted from C to S: your initial S Corp stock basis is your existing C Corp stock basis on the date of the S election.

Stock basis adjusts every year based on the corporation's activity (more on that in the next section).

Debt Basis

This is the often-overlooked second basis bucket. Debt basis represents loans you personally made to the corporation.

It only counts if:

- The loan is from you (the shareholder) directly to the corporation.

- The loan is bona fide (documented, with interest, repayment terms, etc.).

- The loan creates an actual indebtedness from the company to you.

It does not count if:

- The loan is from a bank that you personally guaranteed (guarantor status alone doesn't create debt basis until you actually pay on the guarantee).

- The "loan" is just an undocumented transfer of money with no terms.

- It's a back-to-back loan from a related party.

Debt basis is important because losses can be deducted against both stock basis and debt basis, but distributions can only be received tax-free against stock basis (debt basis doesn't cushion distributions).

How Basis Increases and Decreases (the Famous Order)

Here's the ordering rule that comes up in every basis question. Your stock basis is adjusted in this specific sequence each year:

1. Increases (added in this order):

- Capital contributions you make to the corporation during the year.

- Your share of ordinary income and other separately stated income items (interest, dividends, capital gains, etc.).

- Your share of tax-exempt income.

- Excess depletion deductions.

2. Decreases (subtracted in this order):

- First, distributions to you (but not below zero — distributions in excess of basis are taxable).

- Second, your share of nondeductible expenses and certain other items.

- Third, your share of losses, deductions, and other separately stated loss items.

The ordering matters enormously. Distributions come out before losses are applied, which means a profitable year with both a distribution and a loss can have surprising basis math. The reason for this rule is that the IRS wants to make sure distributions don't accidentally create capital gain just because you had a paper loss in the same year.

If you make an election under Reg. §1.1367-1(g), you can flip the order of #2 and #3 (apply losses before nondeductible expenses), which can be advantageous in some circumstances. Most owners stick with the default.

The AAA: A Different Kind of Account

The Accumulated Adjustments Account (AAA) sounds like basis but is actually a separate corporate-level account, not a shareholder-level account.

AAA tracks the corporation's cumulative net post-S-election profit that has not yet been distributed. It's reported on Schedule M-2 of Form 1120-S.

Why does AAA matter alongside basis?

- AAA determines whether a distribution is tax-free at the corporate level (because it represents already-taxed income).

- For S Corps that have prior C Corp Earnings & Profits (E&P), the AAA-then-E&P ordering determines how distributions are characterized (return of investment vs. taxable dividend).

For S Corps that have always been S Corps (never had a C Corp history with E&P), AAA is mostly a tracking tool — distributions reduce AAA and stock basis in roughly parallel ways, and there's rarely a tax surprise.

The simplest mental model:

- Basis is your personal tax investment in the company. Tracked at the shareholder level.

- AAA is the company's running ledger of post-S-election retained profit. Tracked at the corporate level.

They move together for many transactions but they aren't the same thing, and they can diverge in edge cases (like nondeductible expenses, which reduce stock basis but not AAA).

Form 7203: The Basis-Tracking Form

Starting in 2021, the IRS requires S Corp shareholders to file Form 7203, S Corporation Shareholder Stock and Debt Basis Limitations, with their personal Form 1040 in any year they:

- Claim a loss or deduction from the S Corp.

- Receive a non-dividend distribution.

- Dispose of stock (sell, exchange, or otherwise).

- Receive a loan repayment from the S Corp.

In practice, that's most active S Corp shareholders most years.

Form 7203 walks you through the year's basis math:

- Stock basis at the start of the year.

- Increases for the year (income, contributions).

- Decreases for the year (distributions, then expenses, then losses).

- Stock basis at the end of the year.

- Same for debt basis.

- Computation of allowable losses and deductions (limited to basis).

The form is short — three parts on a single page — but it's not optional. Failure to file when required can result in penalties and can complicate audit defenses if your basis is ever questioned.

The biggest lesson Form 7203 forces: you have to track basis annually, even in years where nothing exciting happens. Tracking it once at year-end during tax prep is much easier than reconstructing 5–10 years of basis history later when you're trying to figure out the gain on a sale.

What Increases Stock Basis (in More Detail)

A more granular list of what bumps your stock basis up:

- Capital contributions — cash or property you put into the company. Property contributions add the property's basis (not its FMV) to your stock basis.

- Ordinary business income — your pro-rata share of the S Corp's ordinary profit.

- Separately stated income — interest income, dividends, capital gains, rental income, etc., that flowed through on your K-1.

- Tax-exempt income — yes, even tax-exempt interest increases your basis.

- Excess depletion — niche, mostly applies to oil/gas/mineral interests.

Any time the company makes money or you put more money in, your basis goes up.

What Decreases Stock Basis

In the IRS's required order:

- Distributions to you (cash or property) — reduce basis dollar for dollar.

- Nondeductible expenses — things like 50% of meal expenses, fines, federal tax penalties, etc. These reduce basis even though they don't show up as deductions on your return.

- Losses, deductions, and credits that flow through to you — ordinary losses, separately stated losses, charitable contributions, Section 179 deductions.

Distributions come out first — even before losses — to make sure distributions don't create accidental capital gains. Once basis hits zero, distributions in excess of basis become capital gains.

A common surprise: nondeductible expenses reduce basis even though they aren't deductible. So a year with a lot of disallowed meals or fines can quietly shrink your basis without giving you any deduction in return.

What Happens When You Take a Distribution in Excess of Basis

This is the most common painful basis surprise for S Corp owners.

Suppose you have $50,000 of stock basis at the start of the year. The corporation has a great year — $200K in profit — but pays out $300K in distributions. Your share of the profit is $100K (50%), and your share of distributions is $150K.

Basis math:

- Starting basis: $50,000

- Plus your share of profit: +$100,000 → basis is now $150,000

- Less distributions: -$150,000 → basis is now $0

- Result: distributions exactly equal basis. No tax surprise.

Now what if the next year, the company has a $0 profit year but still distributes $80,000 to you?

- Starting basis: $0

- Plus profit: $0

- Less distributions: -$80,000 → cannot go below zero

That $80,000 distribution becomes $80,000 of capital gain on your personal tax return. You'll pay long-term capital gains tax (15% or 20% depending on income) on it. That's a $12,000–$16,000 surprise tax bill on a transaction you probably assumed was free.

Avoiding this trap is one of the main reasons to track basis carefully every year and to be conscious of distribution patterns relative to your basis.

What Happens When You Have Losses in Excess of Basis

Mirror image problem. If your S Corp has losses that exceed your basis (stock + debt), the excess losses are suspended — they can't be deducted on your personal return until you have basis to absorb them.

Suspended losses carry forward indefinitely until basis is restored (by future income, capital contributions, or shareholder loans).

This is why owners of distressed or capital-intensive S Corps often have years of suspended losses sitting on their books. They paid the cash for the losses (the company really lost the money) but they can't deduct them yet. When basis is eventually restored, the suspended losses unlock and become deductible.

A Multi-Year Worked Example

Let's track Jason's S Corp basis over five years to see basis in motion.

Year 1 (formation):

Jason starts an S Corp and contributes $30,000 cash for 100% of the stock.

- Starting stock basis: $0

- Capital contribution: $30,000

- Ending stock basis: $30,000

Year 2 (profitable year):

The S Corp earns $80,000 of net income. Jason takes a $20,000 distribution.

- Starting stock basis: $30,000

- Profit: $80,000 → basis is $110,000

- − Distribution: $20,000 → basis is $90,000

- Ending stock basis: $90,000

Year 3 (loss year):

The S Corp loses $40,000. Jason takes no distribution.

- Starting stock basis: $90,000

- − Loss: $40,000 → basis is $50,000

- Ending stock basis: $50,000

The full $40,000 loss is deductible on his personal return because he has plenty of basis.

Year 4 (big distribution year):

The S Corp earns $30,000. Jason takes a $90,000 distribution (financed by drawing down accumulated profits from prior years).

- Starting stock basis: $50,000

- Profit: $30,000 → basis is $80,000

- − Distribution: $90,000 → cannot go below zero

- $10,000 distribution in excess of basis = $10,000 capital gain on Jason's return

- Ending stock basis: $0

Surprise tax bill, even though Jason "thought" the distribution was tax-free.

Year 5 (recovery year):

The S Corp earns $50,000. Jason takes a $20,000 distribution.

- Starting stock basis: $0

- Profit: $50,000 → basis is $50,000

- − Distribution: $20,000 → basis is $30,000

- Ending stock basis: $30,000

Now the $20,000 distribution is tax-free again because basis was restored by the profit.

This is exactly why year-by-year basis tracking matters. Without it, Jason wouldn't have known his basis hit zero at the end of Year 4 and would have been blindsided by the capital gain.

Common Basis Mistakes (Don't Make These)

Mistake 1: Not tracking basis at all. The most common mistake. Owners assume their CPA is tracking it. Some CPAs do, some don't, and many do it only when triggered by a Form 7203 requirement. If you're an S Corp owner, you should know your basis at year-end — every year.

Mistake 2: Treating personal guarantees as debt basis. A common confusion. If you personally guarantee a bank loan to the corporation, that does NOT create debt basis. Debt basis only arises when you actually loan money to the corporation directly (or when you actually pay on the guarantee).

Mistake 3: Forgetting that distributions reduce basis before losses. This ordering rule trips up owners every year. A "loss year with a distribution" can quietly use up your basis on the distribution side and suspend losses you should have been able to deduct.

Mistake 4: Ignoring nondeductible expenses. They still reduce basis, even though they don't give you a deduction. Track them.

Mistake 5: Not filing Form 7203 when required. The IRS has been increasingly strict about Form 7203 compliance. Failure to file when required can lead to disallowance of losses and audit attention.

Mistake 6: Confusing AAA with basis. AAA is a corporate-level account. Basis is shareholder-level. They move together for many transactions but they're not the same. Don't use AAA as a substitute for tracking your own basis.

Mistake 7: Loans from related parties counted as debt basis. If your spouse loans money to the corporation, that doesn't create debt basis for you. The loan must come from you personally to count.

Mistake 8: Not restoring debt basis correctly. When the company repays a shareholder loan that has reduced debt basis, the repayment may have to be partially treated as taxable income. This is a niche but real issue for owners who've moved money in and out as loans.

Mistake 9: Assuming basis carries over on stock transfers. When you transfer S Corp stock (gift, sale, inheritance), the basis story for the recipient is different. Gifts get carryover basis; inherited stock gets stepped-up basis at the date of death; sales create gain/loss for the seller and new cost basis for the buyer.

Mistake 10: Going years without reconciling. Basis math is much harder to reconstruct after the fact. Every additional year you go without reconciling makes the eventual reconstruction more painful and more expensive.

How to Actually Track Basis (Practical Tips)

A few ways to keep basis under control:

- Maintain a basis schedule in a simple spreadsheet — one row per year, columns for starting basis, increases, decreases (in order), and ending basis. Update annually as part of your tax prep.

- Reconcile to your K-1. Every K-1 line that affects basis (income, deductions, distributions, etc.) should be picked up on your basis schedule. The numbers should tie out.

- Save Forms 7203 with your tax records. They are your annual basis snapshot.

- Communicate with your CPA. Ask them explicitly each year: "What's my stock basis and debt basis at year-end?" If they can't answer, that's a problem.

- Audit your loans to the company. Make sure any "loans" you've made are properly documented (note, interest, repayment terms) so they actually create debt basis if challenged.

- Track distributions in real time. Don't wait until year-end to find out you've taken too much.

Basis on the Sale of Your S Corp

When you eventually sell your S Corp shares, basis becomes the foundation for computing your gain or loss. Here's the simplified math:

- Sale price (what you receive)

- − Stock basis (what you've cumulatively invested, adjusted by years of basis changes)

- = Gain or loss on sale

If you've held the shares for more than a year, the gain is generally a long-term capital gain taxed at preferential rates (0%, 15%, or 20% depending on your income).

The key point: higher basis at sale = lower gain = lower tax. So years of disciplined basis tracking, contributions where appropriate, and avoiding unnecessary distribution-driven basis erosion can pay off significantly at exit.

A few sale-time complications worth knowing:

- Asset sale vs. stock sale. Buyers usually prefer to buy the assets of an S Corp (for stepped-up depreciation basis), while sellers usually prefer to sell stock (for cleaner exit and capital gain treatment). The negotiation around structure has direct tax implications for both sides.

- Section 338(h)(10) elections. Allow a stock sale to be treated as an asset sale for tax purposes — a common compromise in S Corp deals.

- Installment sales. If you sell on an installment basis, gain is recognized as you receive payments rather than all at once. Basis is allocated across the payment stream.

- Built-in gains tax. If your S Corp converted from C Corp status within the 5-year recognition period and has appreciated assets being sold, BIG tax can hit at the corporate level.

Sale planning around basis often starts 3–5 years before the actual sale. If you're contemplating a sale, get a CPA involved early.

Inheritance and Basis Step-Up

One of the most powerful estate-planning features of S Corp stock: when an owner dies, their heirs typically receive a stepped-up basis in the inherited shares equal to the fair market value at the date of death.

That can be enormous. If you've built an S Corp with a $50K basis but the company is worth $5M at your death, your heirs inherit shares with $5M basis. If they then sell for $5M, they have $0 of capital gain.

This step-up is one of the reasons sophisticated owners are sometimes counseled to retain their S Corp shares rather than selling during life — the tax savings on death can dwarf what they'd get from a lifetime sale, especially when combined with the federal estate tax exemption.

(There are nuances: the step-up doesn't apply to all assets inside the S Corp the same way it applies to the stock; gift transfers don't get a step-up; estate tax exemption changes can affect planning. This is squarely "talk to an estate planning attorney AND a CPA" territory.)

Frequently Asked Questions

What is S Corp basis in simple terms?

It's a running total of how much money you have invested in your S Corp for tax purposes. It goes up when you put money in or the company earns profit, and down when you take money out or the company loses money.

Why is basis important?

Three big reasons: it limits how much loss you can deduct, it determines whether your distributions are tax-free, and it's used to compute your gain or loss when you eventually sell the business.

How do I find my basis?

Build a basis schedule from formation forward. Each year's K-1 has the inputs you need (income, distributions, etc.). Form 7203 codifies the math. If you've never tracked basis, ask your CPA — but be prepared for them to do a reconstruction project.

What's the difference between basis and AAA?

Basis is at the shareholder level (your investment). AAA is at the corporate level (running balance of post-S-election profits not yet distributed). They move together for many things but they're not the same.

Can my basis go negative?

No. Basis cannot go below zero. Distributions or losses that would push basis negative create capital gains (in the case of distributions) or are suspended (in the case of losses).

Do I have to file Form 7203 every year?

You file it in any year you claim losses, take a non-dividend distribution, dispose of stock, or get a loan repayment. For most active S Corp owners, that's most years.

What's debt basis used for?

Debt basis cushions losses (you can deduct losses against both stock basis and debt basis), but distributions can only be cushioned by stock basis. Debt basis is only available when YOU personally loan money to the corporation.

Does a personal guarantee on a corporate loan create debt basis?

No. Guarantor status alone doesn't count. You only get debt basis if you actually pay on the guarantee or if the loan is directly from you to the corporation.

What happens to basis when I sell my S Corp shares?

Your gain or loss on sale equals the sale price minus your stock basis (with various adjustments for items like ordinary-income recapture, Section 1244 stock treatment, and any loss carryforwards that get released on the sale). This is why basis tracking matters for years before the sale even happens — your gain calculation depends on having a clean, supportable basis schedule. If you've been an S Corp for ten years and never tracked basis, you're going to be reconstructing it under pressure right at the moment you most need a clean number.

The Bottom Line

Basis isn't a clever tax planning concept — it's a running ledger of what's "yours" inside the S Corp for tax purposes. Every dollar of profit increases it; every dollar of distribution or loss decreases it; once it hits zero, the rules change in ways that almost always cost the owner money (surprise capital gains, suspended losses).

The fix is mundane: build a basis schedule from formation, update it with each year's K-1, and file Form 7203 in any year you take a distribution, claim a loss, or sell shares. Your CPA can do this in an hour if your records are clean — or spend ten hours reconstructing it if they're not. Worth doing right.

File Your S Corp Election With FileMyScorp

Basis tracking only matters if your S Corp election is actually on file. Form 2553 is paper-only — no e-file, no IRS online portal — and has to be faxed or mailed to the right service center with every shareholder's signature. FileMyScorp is the cheapest guided 2553 platform on the market, built for owners who want to file it themselves without becoming IRS-routing experts.

- The cheapest pricing in the market. $49 fax · $50 certified mail · $99 for both (same-day). Flat one-time fee, no subscription, no upsells.

- Fax AND certified mail in one place. Most filers do one or the other. We dispatch both same-day, auto-route to the correct IRS service center for your state (Kansas City vs. Ogden), and track delivery on your dashboard.

- DIY-first, no consultation upsell. Owner does the ~10-minute intake. Shareholders e-sign on their phones. We prepare, sign, send.

- Late elections free. Rev. Proc. 2013-30 narrative auto-assembled from a 4-question form — no extra tier, no surcharge.

- Live status from intake → CP261. Every milestone (signed, faxed, delivered, certified-mail tracking, IRS acceptance letter received) hits your inbox and your dashboard.

Start your filing → — most filings go from intake to fax confirmation in under an hour.

Related articles

- May 17, 2026 · 23 minWhat is IRS Form 2553? The Complete 2026 Guide to Filing Your S Corp ElectionForm 2553 made simple. Step-by-step instructions, the 2026 deadline, eligibility rules, late-election relief, where to fax it, and how to avoid the mistakes that get S Corp elections rejected.

- May 16, 2026 · 7 minI got my CP261 letter — now what? (post-election checklist)Got your CP261 acceptance letter? Here's exactly what to do next — payroll setup, tax form changes, deadlines you'll start hitting, and what to put in your records.

- May 15, 2026 · 10 minS Corp vs C Corp in 2026: The $35,000 Question Most Small Business Owners Get WrongS Corp vs C Corp explained for solo owners and small businesses. Real $200k example, when each one wins, the QSBS exit math, and the gotchas your CPA might not mention.