How Is an S Corp Taxed? The Complete Plain-English Guide for 2026

How an S Corp is actually taxed — federal pass-through, state-level treatment, payroll taxes, distributions, K-1s, built-in gains tax, and how owners report it on their personal returns.

If someone told you that an S Corp doesn't pay federal income tax, you'd be forgiven for assuming that S Corps somehow avoid tax altogether. That's not quite right. The corporation itself doesn't pay federal income tax, but every dollar of profit still gets taxed — just on the owner's personal return instead of the company's.

How exactly that works, what the owner's tax bill ends up looking like, where states diverge from the federal rules, and which surprise mini-taxes can hit at the entity level — those are the things most "S Corp 101" articles skip. So we wrote the guide we wished we'd had when we were first untangling this stuff.

This piece walks through how an S Corp is actually taxed, layer by layer: the federal flow-through model, the corporate return, the K-1, the owner's 1040, payroll taxes, distributions, state nuances, the rare entity-level taxes that catch people, estimated payments, and the QBI deduction. With examples. In plain English.

If you've recently elected S Corp status (or you're thinking about it), this is the map.

The 30-Second Version

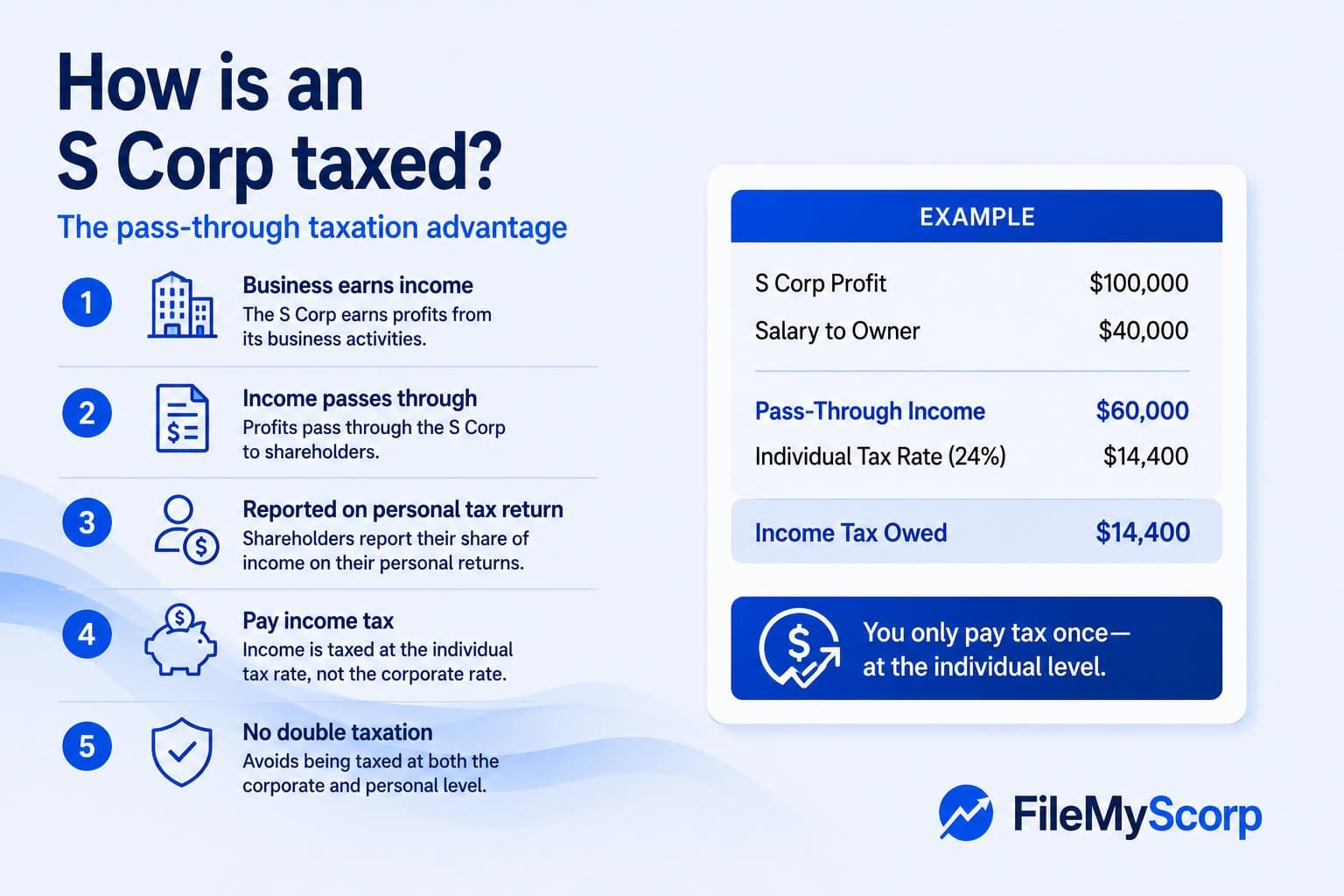

An S Corp is a pass-through entity. That means the business itself doesn't pay federal income tax. Instead, the corporation files an informational return (Form 1120-S), reports its profit, and divides that profit among its owners on Schedule K-1s. Each owner then reports their share of the profit on their personal Form 1040 and pays tax at their own individual rate.

There are three tax flavors involved in running an S Corp:

- Federal income tax, paid by the owners (not the company) on their share of profit.

- Payroll tax, paid on the owner's W-2 wages (not on distributions).

- State tax, which mostly mirrors the federal flow-through model — but with some annoying exceptions.

A small handful of niche entity-level federal taxes can hit S Corps in unusual situations (built-in gains tax, excess net passive income tax). Most owner-operator S Corps never see them.

That's the bird's-eye view. Now let's zoom in.

Layer 1: Federal Income Tax — The Pass-Through Mechanic

S Corps are pass-through entities under Subchapter S of the Internal Revenue Code. The federal income tax on the company's profit is paid by the owners on their personal returns — not by the corporation itself.

Here's the mechanical flow:

- The S Corp earns net income for the year (revenue minus deductible expenses).

- The S Corp files Form 1120-S, U.S. Income Tax Return for an S Corporation, by March 15 (or September 15 with an extension). This is an informational return; the corporation owes no federal income tax on its profit (with rare exceptions noted below).

- As part of that filing, the S Corp issues a Schedule K-1 (Form 1120-S) to each shareholder, allocating their pro-rata share of income, deductions, credits, and other items based on their ownership percentage.

- Each shareholder takes the K-1 and reports the income on their personal Form 1040 (specifically, on Schedule E, Part II).

- The shareholder pays federal income tax on their K-1 income at their personal marginal tax bracket.

A few things to note that surprise new S Corp owners:

You're taxed on your share of the profit whether or not it was distributed to you. This is one of the most common confusions. If your S Corp earned $200K of profit and you only took $80K in distributions, you still pay federal income tax on your full share of the $200K. The remaining $120K stays in the company as retained earnings, and you've already paid tax on it — so when it eventually does come out as a distribution later, it's not taxed again.

This is why S Corp owners need to be very disciplined about setting aside cash for taxes throughout the year. The K-1 doesn't care about your cash flow.

Income, deductions, credits, and special items are reported separately on the K-1. The K-1 isn't just a single number. It breaks out ordinary business income, rental income, interest, dividends, capital gains, charitable contributions, Section 179 depreciation, foreign tax credits, and various other items that need to retain their character for the shareholder's own return.

The K-1 is due to you by March 15. If you're an S Corp shareholder and you haven't received your K-1 by mid-March, your accountant cannot file your personal return on time without it.

Layer 2: Payroll Tax — Wages vs. Distributions

This is where the S Corp's tax magic actually happens.

When you work in your own S Corp, you have to be on W-2 payroll. Your wages are subject to:

- Social Security tax (12.4%) on wages up to the annual wage base (~$176,000 in 2026, indexed for inflation).

- Medicare tax (2.9%) on all wages, with no upper cap.

- Additional Medicare tax (0.9%) on wages above $200K (single) or $250K (joint).

- FUTA (federal unemployment tax) at 0.6% of the first $7,000 of wages.

- SUTA (state unemployment tax) at varying rates by state.

So your salary gets hit with the full 15.3% payroll tax (split between "employer" and "employee" sides on paper, but you're paying both as the owner) — same as if you worked a regular W-2 job.

But here's the upside: distributions don't carry payroll tax. That's the entire point of the S Corp election. The K-1 income that flows to you above and beyond your wages skips the 15.3% payroll layer entirely.

So a $200,000-profit S Corp where the owner takes $100K as wages and $100K as distributions pays:

- $15,300 payroll tax on the $100K wages (~$15.3K)

- $0 payroll tax on the $100K distribution

Compared to a sole prop with the same $200K profit, who would pay roughly $26,800 in self-employment tax. The S Corp owner saves about $11,500 on the payroll tax line alone.

That's why the reasonable comp question matters so much — it's the lever that controls how much of your profit escapes payroll tax. (More on that in our reasonable salary guide.)

Layer 3: State Income Tax — Mostly Pass-Through, Sometimes Not

Most US states honor the federal S Corp election and tax S Corp profits at the owner level (not the corporation). For most owners in most states, the state tax flow looks just like the federal one: K-1 income lands on your personal state return, and you pay tax at your state's individual rate.

But several states have quirks worth knowing:

- California charges a 1.5% franchise tax on S Corp income at the entity level, with a minimum of $800/year. So California S Corps pay both federal-style flow-through and a state-level tax.

- New Hampshire has a Business Profits Tax that doesn't recognize the S election — your S Corp pays state tax at the corporate level.

- Tennessee has an excise tax that applies to S Corps as well.

- Texas has its margin tax (franchise tax), which applies regardless of S election — though many small businesses fall under the no-tax-due threshold.

- New York City taxes S Corps as if they were C corporations for the General Corporation Tax (state-level NY does honor the S election; NYC does not).

- New Jersey requires a separate state-level S Corp election. The federal election alone doesn't carry over.

- Pennsylvania allows S Corp election but lets corporations choose to remain taxed as a C Corp at the state level if they want.

Plus, many states now offer a Pass-Through Entity Tax (PTET) election as a workaround for the federal $10,000 SALT cap. The S Corp pays state tax at the entity level, deducts it federally, and the shareholder gets a state credit. For high-income owners in high-tax states, the PTET election can save real money.

Translation: federal S Corp taxation is mostly a single, predictable model. State S Corp taxation is a patchwork. Always check your state's specific rules.

Layer 4: Distributions — Tax-Free Most of the Time

S Corp distributions are not taxed when they leave the company if they're paid out of profits that have already been taxed at the shareholder level. That's the most common scenario for ongoing S Corps.

Here's the order:

- First, distributions reduce the Accumulated Adjustments Account (AAA) — the running total of post-S-election profit that has been taxed but not yet distributed. If your distribution comes out of AAA, it's tax-free.

- If AAA runs to zero and you have Earnings & Profits (E&P) from C-Corp years (uncommon for businesses that started life as an S Corp), the next layer of distributions is treated as a taxable dividend.

- Once both AAA and E&P are exhausted, distributions are tax-free only to the extent of your basis in the stock.

- Distributions in excess of stock basis are taxable as capital gains.

For most owner-operator S Corps that started life as an LLC or new corporation and elected S status from day one, almost all distributions come out of AAA and are non-taxable events. The big trap is taking out more cash than the business has earned — i.e., distributions in excess of your basis. That triggers capital gains tax.

This is exactly why S Corp owners need to track their basis carefully and file Form 7203 when required. We've written a separate guide on how S Corp basis works that goes deep on this.

Layer 5: The Rare Entity-Level Federal Taxes

Most S Corps never pay any federal income tax at the corporate level. But two niche entity-level taxes can hit:

Built-In Gains Tax (Section 1374)

This applies to corporations that converted from C Corp to S Corp status and still have appreciated assets that were owned during the C Corp years. If those appreciated assets are sold within the 5-year recognition period after the S election, the appreciation that existed at the time of the conversion is taxed at the corporate level at the highest corporate rate (currently 21%).

This is a meaningful issue for businesses that converted from C to S and have valuable real estate, intellectual property, or other appreciated assets. If you've always been an S Corp (or never had C Corp earnings), this doesn't apply to you.

Excess Net Passive Income Tax (Section 1375)

If an S Corp has accumulated E&P from prior C Corp years AND has more than 25% of its gross receipts come from passive sources (interest, dividends, rents, royalties, gain on certain securities), the corporation can owe an entity-level tax on the excess. If this happens for three consecutive years, the S election is automatically terminated.

Again — this is unusual. It mostly hits former C Corps with significant passive investment portfolios. Active operating businesses rarely trip on it.

Estimated Tax Payments

Because S Corp profit flows through to owners but no tax is withheld at the corporate level (only on the W-2 wages), shareholders typically have to make quarterly estimated tax payments on their personal returns to cover the federal and state income tax owed on their K-1 income.

Estimated payments are due:

- April 15 (Q1)

- June 15 (Q2)

- September 15 (Q3)

- January 15 of the following year (Q4)

Underpaying estimated taxes triggers an underpayment penalty. The IRS provides safe harbors — you generally avoid penalties if you've paid at least 100% of last year's federal tax (110% if your AGI was above $150K) or 90% of this year's tax through withholding and estimated payments combined.

Many S Corp owners use a hybrid: they overwithhold federal income tax from their W-2 paycheck (since withholding counts as "paid evenly" throughout the year) to cover the estimated tax owed on their K-1 income. That's a clean way to avoid juggling quarterly checks.

A Worked End-to-End Tax Example

Let's bring all the layers together with one example.

Maya owns an S Corp consulting firm. For 2026:

- Gross revenue: $400,000

- Business expenses (rent, software, contractor payments, etc.): $120,000

- Maya's W-2 salary: $120,000

- Maya's W-2 employer payroll tax (FICA, FUTA): ~$9,500

- Net business income flowing to Maya's K-1: $400K - $120K - $120K - $9.5K ≈ $150,500

What Maya pays in tax on this:

1. On her W-2 salary ($120,000):

- Federal income tax at her marginal bracket — depends on her filing status, deductions, etc. Say roughly $20,000 federal income tax.

- Employee-side payroll tax (Social Security 6.2% up to wage base + Medicare 1.45%): about $9,180 withheld.

- State income tax: depends on state.

2. On her K-1 distribution income ($150,500):

- Federal income tax at her marginal bracket: roughly $35,000 (depending on bracket).

- No payroll tax on the K-1 income.

- Possibly QBI deduction reducing this — let's assume she's under the phase-out and gets a 20% deduction on her qualified portion, saving her ~$6,000–$7,000 in tax.

- State income tax: depends on state.

3. The corporation files Form 1120-S by March 15, 2027, reporting:

- $400K revenue

- $120K business expenses

- $120K wages to Maya

- $9.5K employer payroll tax

- $0 federal income tax owed by the corporation (pass-through)

4. Maya files her personal Form 1040 by April 15, 2027, with:

- W-2 income from her S Corp on Line 1

- K-1 income on Schedule E

- QBI deduction (if eligible) on Line 13

- Tax computed on the total

- Credits for any federal income tax withheld and estimated payments made

This is the "normal" S Corp tax flow. Maya saves about $11,500 in payroll tax compared to operating as a sole prop, gets her QBI deduction, and pays federal/state income tax once (at her personal level) on the full $270K of W-2 + K-1 income.

The QBI Deduction (Section 199A)

Worth its own callout: S Corp owners can qualify for the 20% Qualified Business Income deduction under Section 199A on their personal return. The deduction was made permanent in mid-2025 with 2026 inflation-adjusted phase-out thresholds at roughly $203,000 (single) and $406,000 (married filing jointly).

For S Corp owners specifically:

- The deduction applies to your qualified business income — the K-1 income, after your reasonable W-2 salary is deducted.

- Above the phase-out, the deduction can be limited or eliminated entirely depending on whether your business is a "specified service trade or business" (SSTB) — lawyers, accountants, doctors, financial advisors, consultants, performing artists.

- For non-SSTBs above the phase-out, the deduction depends on W-2 wages and unadjusted basis in business property.

The QBI deduction interacts with your salary decision in a way that matters at higher incomes: a higher W-2 salary reduces the K-1 income that's eligible for QBI. Below the phase-out, this effect is muted; above the phase-out, it can become a major planning factor.

Distributions and Salary Together: What the Owner's Tax Bill Looks Like

Putting payroll tax and income tax together, here's roughly what an S Corp owner pays as a percentage of total business profit:

| Net business profit | Payroll tax (on wages) | Federal income tax (avg) | QBI savings | Approx total tax |

|---|---|---|---|---|

| $80,000 | $7,650 (on $50K salary) | ~$10,000 | ~$1,500 | ~$16,000 |

| $150,000 | $11,475 (on $75K salary) | ~$26,000 | ~$3,500 | ~$34,000 |

| $300,000 | ~$19,000 (on $130K salary) | ~$60,000 | ~$5,500 | ~$74,000 |

| $500,000 | ~$22,000 (on $200K salary, much capped Soc Sec) | ~$120,000 | varies (phaseout) | ~$140,000+ |

These are rough orders of magnitude. Your actual tax depends on filing status, state, deductions, retirement contributions, and lots more. The point is to show how the layering works: payroll tax on a portion, income tax on the whole, with QBI as a shaver-off on top.

Multi-State S Corps: A Quick Word

Once an S Corp does business in more than one state, the tax picture gets more complex. You may have to:

- Register as a foreign entity in each state where you do business — annual report fees, registered agent fees, sometimes additional state-level franchise taxes.

- Apportion your income between states based on each state's apportionment formula (typically some weighted combination of sales, payroll, and property in that state). The result determines how much of your S Corp's income is taxable in each state.

- File state returns in each state — both the S Corp's state-level return and the shareholders' personal nonresident state returns.

- Consider PTET elections in each state that offers them, weighing the federal SALT-cap workaround against the state-by-state mechanics.

For digital and remote businesses, "doing business in" a state can be triggered by relatively modest activity: an employee working remotely, a sales presence above a threshold, a property holding, etc. The rules are fact-specific and increasingly aggressive on the state side. If you have any meaningful multi-state activity, get a CPA who specializes in state and local tax (SALT).

Common Tax Mistakes That Cost S Corp Owners Money

A few patterns we see over and over that quietly erode the tax benefits of the S election:

- Underpaying estimated taxes. Owners get used to having taxes withheld from their W-2 wages and forget that the K-1 income needs estimated payments too. Underpayment penalties stack up fast.

- Forgetting the QBI deduction. Some less-experienced preparers miss the QBI deduction or compute it incorrectly. For a $200K K-1, that's a $40K deduction left on the table — worth thousands in tax.

- Mis-reporting >2% shareholder health insurance. Premiums need to flow through W-2 wages with specific Box 1/Box 3/Box 5 treatment to be deductible. Miss the reporting and the deduction is lost.

- Misclassifying owner draws as wages or vice versa. Distributions and wages are separate, and reclassifying them after the fact creates audit risk and accounting headaches.

- Skipping the basis tracking. As covered in our S Corp basis guide, distributions in excess of basis trigger surprise capital gains. Owners who don't track basis get blindsided.

The fix for almost all of these is the same: a competent CPA, clean books, real payroll, and a tax planning conversation in November (not in March when it's too late to adjust).

Frequently Asked Questions

Does the S Corp itself pay federal income tax?

In nearly all cases, no. The corporation files an informational Form 1120-S, but the income is taxed on each shareholder's personal return. The two exceptions are the built-in gains tax and the excess net passive income tax, both of which are uncommon for typical owner-operator S Corps.

Are S Corp distributions taxed?

Generally no — distributions to the extent of your AAA and stock basis are tax-free, because the underlying profit was already taxed on your K-1. Distributions that exceed your basis are taxed as capital gains.

How is an S Corp owner's salary taxed?

Just like any W-2 salary: income tax withheld at your marginal rate, plus the full 15.3% payroll tax (Social Security + Medicare), plus state income tax where applicable. The owner pays both halves of the payroll tax (the "employer" half via the corporation's deduction, and the "employee" half via withholding).

Do I pay self-employment tax as an S Corp owner?

No — S Corp owners don't pay self-employment tax in the traditional sense. They pay payroll tax on their W-2 wages instead. The functional difference: only your wages are subject to that 15.3%, not your distributions.

Will an S Corp save me income tax?

The S Corp election primarily saves you payroll/SE tax, not income tax. Your overall income tax may shift slightly because of how the wages and distributions interact with deductions and the QBI calculation, but the headline savings are payroll-tax savings.

When are S Corp tax returns due?

Form 1120-S (the corporate informational return) is due March 15 each year, with an automatic 6-month extension available via Form 7004 (extending to September 15). K-1s should be issued to shareholders by March 15. Owners then file their personal returns by April 15.

How are S Corp losses treated?

Losses pass through to owners on the K-1 and can offset other personal income — but only up to the owner's stock and debt basis. Losses in excess of basis are suspended and carried forward until basis is restored.

What's the difference between an S Corp distribution and a dividend?

For tax purposes within the S Corp world, "distribution" is the more accurate term. Distributions reduce AAA and stock basis. Only when an S Corp has C Corp Earnings & Profits from prior years can a distribution be reclassified as a taxable dividend — uncommon for businesses that've always been S Corps.

Do S Corps pay state taxes?

Most states honor the federal S Corp pass-through treatment, so the state tax is paid by the owners on their personal returns. A handful of states (CA, NH, TN, TX, NJ, NYC) have entity-level taxes or quirky state rules that affect S Corps. Always check your state.

What if my S Corp has multiple shareholders?

Each shareholder receives a K-1 with their pro-rata share (based on ownership %) of every income, deduction, and credit item. They each report their share on their own Form 1040 and pay tax at their own personal rates. S Corps cannot allocate income disproportionately like LLCs taxed as partnerships can.

Are health insurance premiums taxed?

Health insurance premiums paid by the corporation for shareholders owning more than 2% must be reported as W-2 wages (in Box 1, but excluded from boxes 3 and 5 for Social Security and Medicare). The shareholder then deducts the premiums "above the line" on their personal 1040 as a self-employed health insurance deduction. Net effect: no income tax on the premiums, but they must show up on the W-2 — or the deduction is disallowed.

The Bottom Line

S Corp taxation is a structural shift, not a magic trick. The corporation files an informational 1120-S; the income flows through to your K-1; your salary is taxed like any W-2 wage; your distributions are tax-free up to your basis; and the QBI deduction can shave another 20% off the income side if you qualify.

The savings come from one specific lever: splitting your business income between W-2 wages and distributions, so only the wages get hit with payroll tax. Set the salary at a defensible reasonable-comp number, track your basis every year on Form 7203, file 1120-S on time, and the election does most of its work in the background — quietly converting what would have been self-employment tax into either retirement contributions or your bank account.

File Your S Corp Election With FileMyScorp

The tax math only matters if your election is actually on file with the IRS. Form 2553 is paper-only — no e-file, no online portal — and has to be faxed or mailed to the right service center with every shareholder's signature. FileMyScorp is the cheapest guided 2553 platform on the market, built for owners who want to file it themselves without becoming IRS-routing experts.

- The cheapest pricing in the market. $49 fax · $50 certified mail · $99 for both (same-day). Flat one-time fee, no subscription, no upsells.

- Fax AND certified mail in one place. Most filers do one or the other. We dispatch both same-day, auto-route to the correct IRS service center for your state (Kansas City vs. Ogden), and track delivery on your dashboard.

- DIY-first, no consultation upsell. Owner does the ~10-minute intake. Shareholders e-sign on their phones. We prepare, sign, send.

- Late elections free. Rev. Proc. 2013-30 narrative auto-assembled from a 4-question form — no extra tier, no surcharge.

- Live status from intake → CP261. Every milestone (signed, faxed, delivered, certified-mail tracking, IRS acceptance letter received) hits your inbox and your dashboard.

Start your filing → — most filings go from intake to fax confirmation in under an hour.

Related articles

- May 17, 2026 · 23 minWhat is IRS Form 2553? The Complete 2026 Guide to Filing Your S Corp ElectionForm 2553 made simple. Step-by-step instructions, the 2026 deadline, eligibility rules, late-election relief, where to fax it, and how to avoid the mistakes that get S Corp elections rejected.

- May 16, 2026 · 7 minI got my CP261 letter — now what? (post-election checklist)Got your CP261 acceptance letter? Here's exactly what to do next — payroll setup, tax form changes, deadlines you'll start hitting, and what to put in your records.

- May 15, 2026 · 10 minS Corp vs C Corp in 2026: The $35,000 Question Most Small Business Owners Get WrongS Corp vs C Corp explained for solo owners and small businesses. Real $200k example, when each one wins, the QSBS exit math, and the gotchas your CPA might not mention.