Can an LLC Be Owned by an S Corp? (Yes — Here's How It Works in 2026)

Can an S Corp own an LLC? Yes, and there are smart reasons to do it. A plain-English guide to single-member LLC subsidiaries, multi-member LLCs, QSubs, holding company structures, and the mistakes to avoid.

This question comes up constantly, usually right around the time a successful business owner starts thinking about a second venture, a real estate investment, or a holding company structure: can my S Corp own an LLC?

The short answer is yes — and not only is it allowed, it's a common structure used by smart small business owners to separate liability across ventures, hold real estate, segregate brand identities, or set up holding companies. But there are several flavors of "S Corp owning an LLC," each with different tax consequences, and a couple of common mistakes that can quietly create big tax problems.

This guide walks through every variation: single-member LLC subsidiaries (the most common), multi-member LLC subsidiaries, LLCs that elect to be taxed as corporations, and Qualified Subchapter S Subsidiaries (QSubs). It also tackles the reverse question — can an LLC own an S Corp? — because the answer is much more restrictive and trips people up.

If you're considering layering an LLC under your existing S Corp, this is the map. We synthesized what the most-watched S Corp YouTube channels and tax/legal blogs cover, plus the IRS's own guidance, into one usable guide.

The 60-Second Version

Can an S Corp own an LLC? Yes — in three flavors:

- Single-member LLC owned by an S Corp. The LLC is treated as a "disregarded entity" for federal tax purposes. All its income and expenses flow up to the parent S Corp's books and onto the S Corp's 1120-S.

- Multi-member LLC owned by an S Corp + others. The LLC is taxed as a partnership. The S Corp gets a K-1 from the LLC, which flows up onto the S Corp's 1120-S as separately stated items.

- LLC that has elected to be taxed as a corporation, owned by an S Corp. The LLC is treated as a separate corporation and files its own corporate return.

There's also a special creature called a Qualified Subchapter S Subsidiary (QSub), which is technically a corporation owned 100% by an S Corp parent and treated as disregarded for federal tax. We'll cover that too.

The reverse — can an LLC own an S Corp? — is much more restricted. Generally, no, because LLCs aren't on the IRS's list of eligible S Corp shareholders. There are very narrow workarounds, but they're rare.

Let's go through each scenario.

Scenario 1: An S Corp Owns a Single-Member LLC (the Most Common Setup)

This is the structure most owners ask about. You have an existing S Corp, and you want to set up a new LLC for a related business activity — a second brand, a real estate property, a side project, an asset-holding entity — and have your S Corp own 100% of it.

This is allowed, and it's actually quite clean from a tax standpoint.

How the IRS treats it: A single-member LLC owned by an S Corp is, by default, a disregarded entity for federal tax purposes — meaning the IRS pretends the LLC doesn't exist and just folds its activity up into the parent S Corp's tax return. There's no separate federal tax return for the LLC. All of its income, deductions, and assets are reported on the S Corp's Form 1120-S.

Why owners do it:

- Liability separation. Each LLC subsidiary creates a legal box around its activity. If one venture gets sued, the other ventures' assets (and the parent S Corp's assets) are generally protected.

- Brand or operational separation. Different brands, different DBAs, different customer-facing identities — without creating tax complexity.

- Asset protection. Holding valuable assets (a building, a piece of equipment, IP) in a separate LLC owned by the S Corp keeps those assets protected from operational liabilities.

- Future flexibility. An LLC subsidiary can later be sold, brought in new investors (converting to multi-member LLC, taxed as partnership), or converted to a different structure with relative ease.

Tax filing:

- The S Corp files Form 1120-S as usual.

- The LLC subsidiary files no separate federal tax return.

- The LLC's revenue, expenses, assets, and liabilities are reported on the S Corp's 1120-S — though most CPAs maintain separate books for each LLC for record-keeping clarity.

- Some states still require the LLC to file a state return or pay a state-level fee even though it's federally disregarded (California is the obvious example — your single-member LLC subsidiary will still pay the $800 minimum LLC tax).

Liability:

- The LLC creates a legal shell that protects the parent S Corp's other assets from the LLC's liabilities, and vice versa, if you maintain corporate formalities (separate bank accounts, separate contracts, no commingling).

This is the cleanest, most common structure for an S Corp owner who wants to layer in additional ventures.

Scenario 2: An S Corp Owns a Multi-Member LLC (with Other Owners)

What if your S Corp wants to partner with another person or business to form an LLC together?

How the IRS treats it: A multi-member LLC is, by default, taxed as a partnership for federal tax purposes — regardless of whether one of the members is an S Corp.

So you'd have:

- The new LLC files its own Form 1065 (partnership return) annually.

- The LLC issues a Schedule K-1 to each member, including your S Corp.

- Your S Corp picks up its share of the LLC's income, deductions, and credits from the K-1 and includes them on its own 1120-S.

- The S Corp shareholders (you and any other S Corp owners) then pick up their share of those items via their personal K-1s from the S Corp.

This is a tax-stack-on-tax-stack — perfectly legal and not double-taxed (everything is pass-through), but more complex on the paperwork side.

Why owners do it:

- The S Corp can be a partner in a venture without that venture having to be its own S Corp.

- Other partners in the LLC can be ineligible S Corp shareholders (foreign persons, corporations, partnerships) without creating an S Corp problem — because they're investing in an LLC, not in the S Corp.

- Allows flexible profit-sharing arrangements within the LLC (LLCs can allocate profits disproportionately; S Corps can't), while preserving the S Corp's payroll tax savings on the income flowing back up.

A common use case:

A successful S Corp consulting firm wants to invest in a real estate project with two other investors. Rather than having all three owners directly own real estate (or trying to fit the deal inside the S Corp, which is usually a tax disaster for real estate), they form a new LLC for the property. The S Corp is one of the LLC members, and the other two investors are the other members. The LLC files Form 1065 each year, the S Corp gets a K-1, and the rental income/depreciation flows up cleanly.

Scenario 3: An S Corp Owns an LLC That Has Elected to Be Taxed as a Corporation

This is rare but worth mentioning. An LLC can affirmatively elect (via Form 8832 or by filing Form 2553 to be taxed as an S Corp) to be taxed as a corporation rather than the default disregarded entity / partnership treatment.

If your S Corp owns an LLC that has made such an election:

- If the LLC elected C Corp treatment: The LLC files its own Form 1120 (C Corp return) and pays its own corporate tax. Your S Corp's ownership in the LLC is treated like any other corporate stock investment.

- If the LLC elected S Corp treatment: This usually doesn't work because S Corps cannot own other S Corps directly (with the QSub exception covered below). An ownership structure that tries to put an S Corp under another S Corp typically violates eligibility rules.

This scenario is uncommon for owner-operator small businesses. It's more often seen in larger multi-entity structures with specific tax planning goals.

Scenario 4: The QSub — A Corporation Owned 100% by an S Corp

Now we get into a special creature: the Qualified Subchapter S Subsidiary, or QSub.

A QSub is a corporation (typically a state-law corporation, sometimes an LLC that has elected corporate treatment) that is:

- 100% owned by a single S Corp parent.

- Eligible to be an S Corp itself.

- Has had a QSub election filed for it via Form 8869, Qualified Subchapter S Subsidiary Election.

When properly elected, the QSub is treated as a disregarded entity for federal tax purposes — its assets, liabilities, income, deductions, and credits all flow up to the parent S Corp's 1120-S, just like a single-member LLC subsidiary.

Why does the QSub exist? Because S Corps generally can't own other S Corps directly. The QSub election was created so that an S Corp could own a corporate subsidiary (and have it be tax-disregarded) without the eligibility problem.

Practical comparison: QSub vs. Single-Member LLC owned by an S Corp

For most small business owners, these two structures are functionally similar — both result in a disregarded subsidiary that folds up into the parent S Corp's books. The choice usually comes down to:

- State law preferences. Some states have specific rules or tax preferences that favor corporations vs. LLCs.

- Future flexibility. A single-member LLC can easily convert to multi-member (partnership treatment) if you want to bring in investors. A QSub election is harder to undo cleanly.

- Filing costs. A QSub requires filing Form 8869; an LLC subsidiary just needs to be formed at the state level. The LLC route is usually simpler.

For most owner-operators, forming a single-member LLC under the S Corp is simpler and more flexible than the QSub route. The QSub is more commonly used for legacy structures or when there's a specific reason to use a corporation rather than an LLC.

Scenario 5: A Holding Company Structure

Many growing S Corp owners eventually consider a holding company structure: one parent S Corp, multiple LLC subsidiaries, each holding a different line of business or asset class.

A typical structure:

- Parent: ABC Holdings S Corp — owned by you.

- Subsidiary 1: ABC Operations LLC — single-member LLC owned by the S Corp, runs the main operating business.

- Subsidiary 2: ABC Real Estate LLC — single-member LLC owned by the S Corp, holds the office building the operating business uses.

- Subsidiary 3: ABC Equipment LLC — single-member LLC owned by the S Corp, holds vehicles and equipment.

All three subsidiaries are disregarded entities for federal tax. They file no separate federal return; everything rolls up to the parent S Corp's 1120-S. But each subsidiary creates a legal liability box around its activities.

Benefits of this structure:

- Operational liability is contained inside the operating LLC. If a customer sues over a service issue, only the operating LLC's assets are exposed (not the real estate, not the equipment).

- The real estate LLC charges rent to the operating LLC (an internal transaction). Internally, this is effectively just a wash, but for liability and accounting reasons it creates clean separation.

- Future growth is easier — selling a single subsidiary is cleaner than carving up a single mega-entity.

- Bringing in outside investors at the subsidiary level (without restructuring the parent S Corp) is easier.

Drawbacks:

- More entities to maintain. Each subsidiary has its own state filing requirements, registered agent, annual report, possible state-level fees.

- Slightly more complex bookkeeping (though the federal tax filing is still just the one 1120-S).

- Some states tax single-member LLCs even when federally disregarded (e.g., California's $800 minimum tax per LLC adds up fast in a multi-LLC holding structure).

For owners with multiple distinct business lines or significant assets, the holding company structure pays off the modest extra complexity. For single-business owner-operators, it's usually overkill.

A Real-World Example: Real Estate Investor + Operating Business

Maya runs a successful S Corp consulting firm, which nets her about $300K per year. She wants to buy a small office building — partly to use for her own business, partly to rent out the extra space to other tenants.

Bad option: Have the S Corp itself buy the building. Real estate inside an S Corp is generally a tax disaster — depreciation can't be optimized, distribution flexibility is limited, and the eventual sale or refinancing creates ugly tax consequences.

Better option: Have Maya personally own a separate single-member LLC that holds the real estate. The LLC charges fair-market rent to her S Corp for the office space. The LLC's rental income (and depreciation) flows to her personally on Schedule E.

Best option (depending on circumstances): Have Maya's S Corp own a single-member LLC that holds the real estate. The S Corp gets the liability separation between operations and real estate. The real estate's depreciation flows up onto the S Corp's 1120-S, where Maya can use it as a deduction. The S Corp pays rent to the real estate LLC (internal wash) but the structure is clean for liability purposes.

The "best" structure depends on Maya's specific tax situation — whether she wants the rental losses to flow to her personal return (separate LLC) vs. up to the S Corp (LLC subsidiary). This is exactly the sort of question worth a CPA conversation.

(Note: holding rental real estate inside an S Corp directly is generally bad. Holding it in a separate disregarded LLC owned by the S Corp is more nuanced and depends on the facts.)

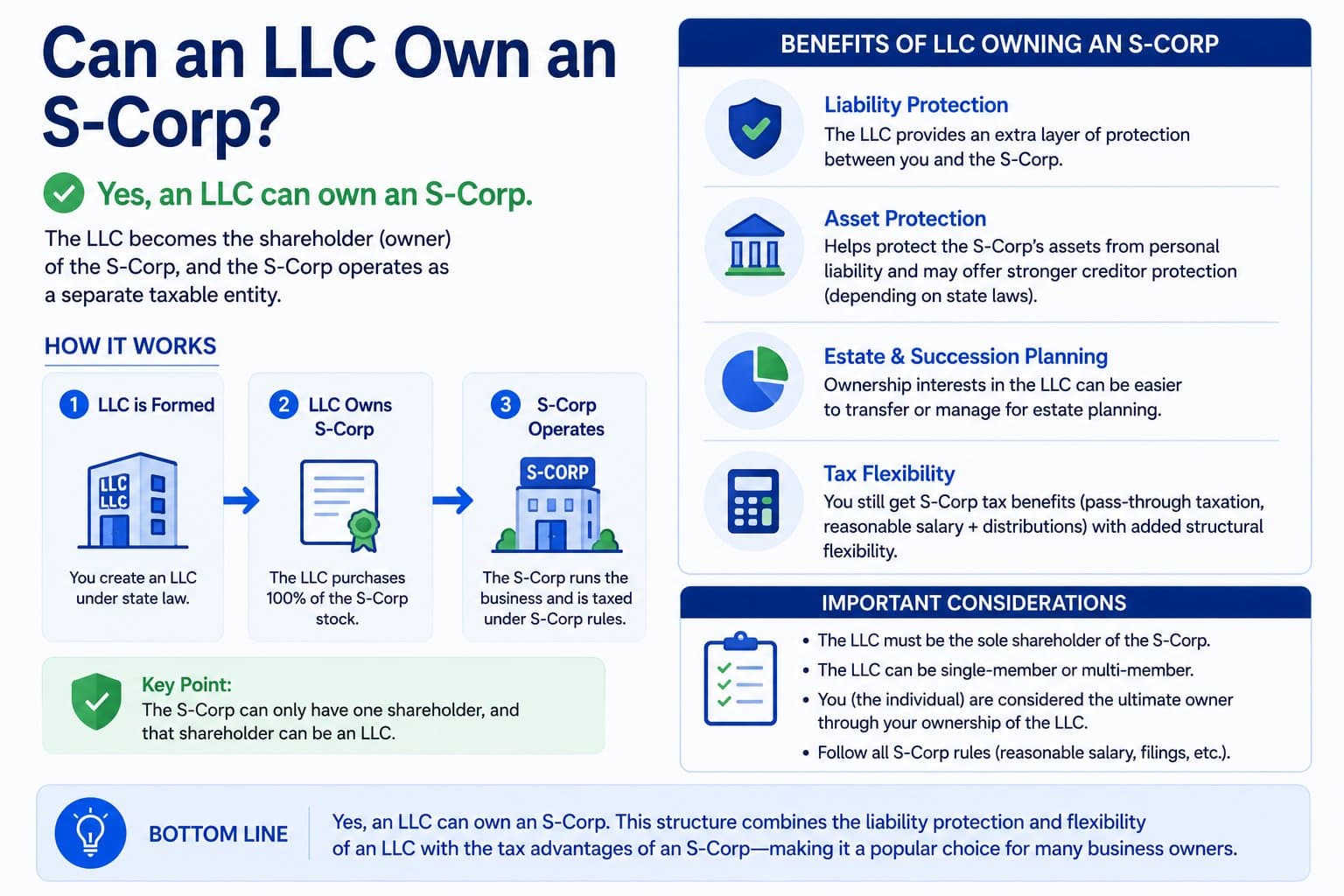

The Reverse Question: Can an LLC Own an S Corp?

This is where things get restrictive.

The general answer is no. S Corps have strict eligibility rules about who can be a shareholder:

- US individuals (citizens or residents).

- Certain estates.

- Certain trusts (grantor trusts, QSSTs, ESBTs, voting trusts, certain retirement and 501(c)(3) trusts).

LLCs are not on the list. Neither are partnerships, foreign individuals or entities, or most corporations. So a standard LLC cannot own S Corp stock — full stop.

There are a couple of niche exceptions:

- A single-member LLC owned by an eligible US individual can technically be a "shareholder" of an S Corp because the IRS disregards the LLC for tax purposes and treats the underlying owner as the actual shareholder. So functionally, the eligible US individual owns the S Corp through their disregarded SMLLC. (Most CPAs avoid this structure because it adds complexity for no real tax benefit.)

- A QSub structure, where an S Corp parent owns 100% of another corporation that has a QSub election in place — but this is the S Corp owning the corporation, not the other way around.

What if you accidentally have an LLC own S Corp stock? The S Corp election can be inadvertently terminated, with serious tax consequences (loss of S status, potential immediate corporate tax). If this comes up — for instance, an estate plan that puts S Corp stock into an LLC for "asset protection" — get a tax pro involved immediately. There may be relief options (Rev. Proc. 2013-30, inadvertent termination relief, etc.) but they require quick action.

The simple rule for owners: don't put your S Corp stock into an LLC without specific, sophisticated tax advice.

Common Mistakes to Avoid

Mistake 1: Putting real estate inside the S Corp itself rather than in a subsidiary LLC. Real estate inside an operating S Corp is generally a bad fit. Use a separate LLC (either owned by you personally or by your S Corp as a disregarded subsidiary).

Mistake 2: Letting a single-member LLC subsidiary "elect" to be taxed as an S Corp. This usually doesn't work because S Corps can't own other S Corps directly. If you want corporate disregarded treatment under your S Corp, use a QSub election or just leave the LLC as a default-treatment SMLLC.

Mistake 3: Putting an LLC as a shareholder of your S Corp. Generally not allowed, and can terminate your S election. Be careful with estate plans, trust structures, and ownership transfers.

Mistake 4: Forgetting that disregarded subsidiaries still have state filing obligations. Federal disregarded ≠ state disregarded. California, in particular, charges its $800 minimum LLC tax on every single-member LLC, regardless of federal treatment.

Mistake 5: Commingling funds across the parent and subsidiaries. If you don't maintain clean separation (separate bank accounts, separate contracts, separate insurance policies), you can pierce the corporate veil and lose the liability protection that motivated the structure in the first place.

Mistake 6: Not formalizing intercompany transactions. If your S Corp pays rent to its real estate LLC subsidiary, that should be documented with a written lease at fair market terms. Otherwise, in an audit, the IRS may recharacterize the payments.

Mistake 7: Over-engineering the structure. Not every S Corp owner needs a holding company with five subsidiaries. Sometimes a single S Corp does just fine. Add complexity only when there's a clear reason.

Mistake 8: Setting up the structure without thinking about exit. When you eventually sell the business, the structure matters — buyers prefer some structures over others. Plan with the exit in mind, not just the day-to-day operations.

Frequently Asked Questions

Can an S Corp own an LLC?

Yes. An S Corp can own a single-member LLC (treated as a disregarded entity), be a member of a multi-member LLC (treated as a partnership), or own an LLC that has elected corporate treatment. All three are allowed.

Can an S Corp own 100% of an LLC?

Yes. A single-member LLC owned 100% by an S Corp is treated as a disregarded entity for federal tax purposes — its income and expenses flow up to the parent S Corp's 1120-S.

Can an S Corp be a partner in an LLC?

Yes. An S Corp can be a partner (member) in a multi-member LLC taxed as a partnership. The S Corp receives a K-1 from the LLC and reports its share of income and deductions on its own 1120-S.

Does an S Corp owning an LLC create double taxation?

No. Because the LLC subsidiary is either disregarded (single-member) or a partnership (multi-member), all income flows through to the S Corp without an entity-level tax at the LLC level. The S Corp itself is also a pass-through. So there's no double tax.

Does an LLC owned by an S Corp file its own tax return?

A single-member LLC owned by an S Corp typically files no separate federal return — it's disregarded. A multi-member LLC owned by the S Corp and others files Form 1065 (partnership return). An LLC that has elected corporate treatment files its own corporate return.

Can an LLC own an S Corp?

Generally no. LLCs aren't on the IRS's list of eligible S Corp shareholders. The narrow exception: a single-member LLC owned by an eligible US individual can technically own S Corp stock because the LLC is disregarded and the individual is treated as the real owner. Most other LLC ownership structures terminate the S election.

What's the difference between a QSub and an LLC subsidiary owned by an S Corp?

Functionally similar — both result in a disregarded subsidiary whose activity flows up to the parent S Corp. A QSub requires an active election (Form 8869) and only applies to corporations. A single-member LLC subsidiary is automatically disregarded by default (no election needed) and can be more flexible if you later want to bring in additional members.

What's the best structure for holding real estate inside an S Corp?

Generally: don't. Hold the real estate in a separate single-member LLC, either owned by you personally or owned by the S Corp as a subsidiary. This preserves depreciation flexibility, avoids ugly tax consequences on eventual sale, and creates clean liability separation.

Can my S Corp own multiple LLCs?

Yes. A common holding company structure has one S Corp parent owning multiple disregarded LLC subsidiaries — each holding a different line of business, asset, or geography.

Do I need a Form 8832 to elect disregarded treatment for an LLC owned by my S Corp?

No. Single-member LLCs are disregarded by default for federal tax purposes — no form needed. Form 8832 is only required if you want to opt out of the default treatment (e.g., elect corporate treatment instead).

If my S Corp owns an LLC, can the LLC have non-US members?

The S Corp itself can't have non-US shareholders, but the LLC subsidiary can have non-US members if it's a multi-member LLC taxed as a partnership. The S Corp would just be one of the LLC's members.

Does the S Corp's reasonable comp requirement extend to its LLC subsidiaries?

Yes, indirectly — the work performed by the S Corp owner for the LLC subsidiaries is still work for the parent S Corp's broader business, and the salary should reflect total responsibilities across all entities.

Can I move assets from my S Corp to a subsidiary LLC tax-free?

Generally yes. A contribution of assets from an S Corp to a wholly owned disregarded subsidiary LLC is treated as a non-event for federal tax purposes (the S Corp still owns the assets, just through a disregarded LLC wrapper). Caveats apply for some asset types and for moves that change the ultimate ownership.

The Bottom Line

Yes, an S Corp can own an LLC — and for many owners, it's a smart move that adds liability separation, brand flexibility, and asset protection without creating tax complexity. The single-member LLC subsidiary is the simplest and most common version: federally disregarded, cleanly folded into the parent S Corp's tax return, with clean legal separation as long as you maintain formalities.

Multi-member LLC partnerships under your S Corp are also fine — just slightly more complex on the tax filing side.

The reverse is much more restrictive: an LLC generally cannot own an S Corp without terminating the election. Be careful with estate plans and trust structures that touch S Corp stock.

For most growing S Corp owners, layering in a disregarded LLC subsidiary at the right moment — when you're acquiring real estate, launching a second brand, or holding a significant asset — is one of the most useful structural moves you can make. Just make sure the structure matches your tax goals, you maintain clean separation between entities, and you have a CPA in the loop before pulling the trigger.

File Your S Corp Election With FileMyScorp

The S-Corp-owns-LLC structure works best when the underlying S Corp election was filed cleanly and on time in the first place. If you haven't filed Form 2553 yet — or you elected late and need Rev. Proc. 2013-30 relief — that's the place to start before you start layering in subsidiaries. FileMyScorp is the cheapest guided 2553 platform on the market, built for owners who want to file it themselves without becoming IRS-routing experts.

- The cheapest pricing in the market. $49 fax · $50 certified mail · $99 for both (same-day). Flat one-time fee, no subscription, no upsells.

- Fax AND certified mail in one place. Most filers do one or the other. We dispatch both same-day, auto-route to the correct IRS service center for your state (Kansas City vs. Ogden), and track delivery on your dashboard.

- DIY-first, no consultation upsell. Owner does the ~10-minute intake. Shareholders e-sign on their phones. We prepare, sign, send.

- Late elections free. Rev. Proc. 2013-30 narrative auto-assembled from a 4-question form — no extra tier, no surcharge.

- Live status from intake → CP261. Every milestone (signed, faxed, delivered, certified-mail tracking, IRS acceptance letter received) hits your inbox and your dashboard.

Start your filing → — most filings go from intake to fax confirmation in under an hour.

This article is general educational information, not tax, legal, or financial advice for your specific situation. Tax law changes, your facts matter, and what's right for one business may be wrong for another. Always confirm with a qualified CPA, EA, or attorney before designing entity structures or making structural decisions.

Related articles

- May 17, 2026 · 23 minWhat is IRS Form 2553? The Complete 2026 Guide to Filing Your S Corp ElectionForm 2553 made simple. Step-by-step instructions, the 2026 deadline, eligibility rules, late-election relief, where to fax it, and how to avoid the mistakes that get S Corp elections rejected.

- May 16, 2026 · 7 minI got my CP261 letter — now what? (post-election checklist)Got your CP261 acceptance letter? Here's exactly what to do next — payroll setup, tax form changes, deadlines you'll start hitting, and what to put in your records.

- May 15, 2026 · 10 minS Corp vs C Corp in 2026: The $35,000 Question Most Small Business Owners Get WrongS Corp vs C Corp explained for solo owners and small businesses. Real $200k example, when each one wins, the QSBS exit math, and the gotchas your CPA might not mention.